Chat with us at LMA 2026: Booth 201

Frogs, Whales, and Long Tails: Key Takeaways from the LMA 2026 AI Pre-Conference:

Michelle Woodyear

Frogs, Whales and Long Tails

Takeaways from "Legal Industry Intelligence: Data Futurists Reveal What's Next" at the LMA 2026 Annual Conference Pre-Conference Program, AI, BI, CI: The ABCs of Data and Law Firm Intelligence.

Speakers: Jen Dezso, Thomson Reuters Institute; Quynh Skiven, Epiq; and Robert Ambrogi, LawNext Media. Moderated by Michelle Woodyear, Mount Insights.

Key Takeaways

1-The headline numbers look good. The underlying data does not.

Rate growth remains strong, but it's doing less of the heavy lifting it used to. Underneath the surface: declining billable hours, write-offs up sharply, aged work-in-progress becoming the top cash flow pressure, and clients shifting work downstream. The traditional model is being propped up, not fundamentally strengthened.

2-Firms have a focus problem, not a depth problem.

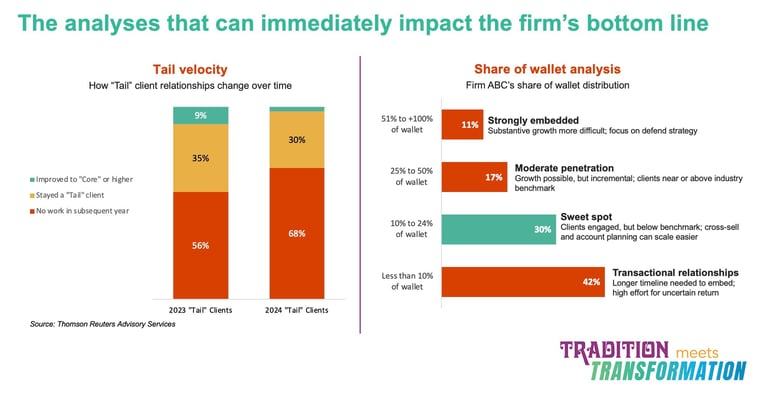

Only 23% of outside counsel spend goes to the firm a client uses the most. The sweet spot for growth sits with clients where your firm handles 10-24% of their legal spend, but most firms chase whale clients where they're already deeply embedded or tail clients who will never meaningfully grow.

3-Data strategy is a people and culture problem, not a technology problem.

95% of AI pilots fail to deliver on expectations, and the primary reason is not the technology itself. It's dirty data, disconnected systems, and a lack of organizational buy-in. Firms that skip the foundational data work will spend multiples of the time and money cleaning up later.

4-The competitive landscape has changed in ways most firms haven't internalized.

AI-native law firms, management service organizations backed by private equity, alternative legal service providers, and increasingly sophisticated in-house legal departments are all reshaping how legal services are delivered and purchased. The window to adapt is shorter than it feels.

5-The question is not whether your firm will be reshaped. It's whether your firm will be the one doing the reshaping.

Whales, frogs, and long tails. If anyone asks what you learned today, just tell them LMA is pivoting to wildlife programming.

The Design of the Session

This was the capstone of the pre-conference day, intentionally positioned after sessions on CI fundamentals, advanced intelligence workflows, and AI tools in action. The goal was directional: not tactics, not a tools demo, but a conversation about structural shifts in the legal market and what they demand from firm leadership.

The session was structured in three acts.

Act One covered signals: what is the data telling us about the state of the market, both the bright spots and the dark spots?

Act Two explored structural implications: if these signals accelerate over the next three to five years, what changes in the business model, talent, pricing, and client relationships?

Act Three focused on moves: what should leaders prioritize in the next six to twelve months?

Three speakers brought three distinct lenses.

Jen Dezso from the Thomson Reuters Institute brought the financial data and client analytics.

Quynh Skiven from Epiq brought the data architecture and governance perspective.

Robert Ambrogi from LawNext Media brought the competitive landscape and industry analysis.

Jen Dezso is a market analyst at the Thomson Reuters Institute. Her role was to set the stage with data, and the data told a more complicated story than most firm leaders want to hear.

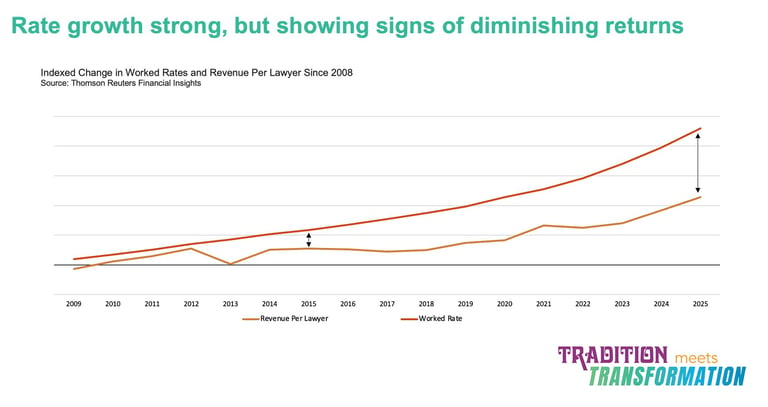

She opened with rate growth. For the past decade, rate increases have been doing most of the heavy lifting for law firm revenue. And on the surface, that trend continues. But the chart she showed revealed something important: the gap between rate growth and revenue-per-lawyer growth is widening. Rates are going up, but they're producing less incremental value than they used to. The link between pricing and growth is loosening.

For marketing and BD teams, this matters because it changes the internal narrative. If leadership believes pricing alone will continue to bail out growth targets, there's less urgency to change behavior elsewhere. But when rate increases stop compounding growth on their own, firms face harder questions about client portfolio, effort allocation, and where to focus.

Except most firms aren't asking those questions. Jen shared research from interviews with more than 100 managing partners. The most frequently discussed growth strategies were laterals, mergers, and geographic expansion. Client relationships and cross-selling were at the bottom of the list. Not because clients aren't important, she argued, but because client growth is harder. It's messier, slower, and requires more internal coordination than hiring a lateral. So it gets pushed to marketing and BD teams, often too late, and usually as a tactical exercise rather than a strategic one.

The client data reinforced this. Only 23% of a client's outside counsel spend goes to the firm they use the most. The average primary relationship covers fewer than three types of work, and the median is between one and two practice areas. Only 15% of clients plan to increase the work they send to their most-used firm. Jen's read: firms don't have a depth problem. They have a focus problem. Growth isn't blocked by a lack of opportunity. It's blocked by not knowing which relationships are expandable and which aren't.

Jen Dezso: The Numbers Behind the Growth Story

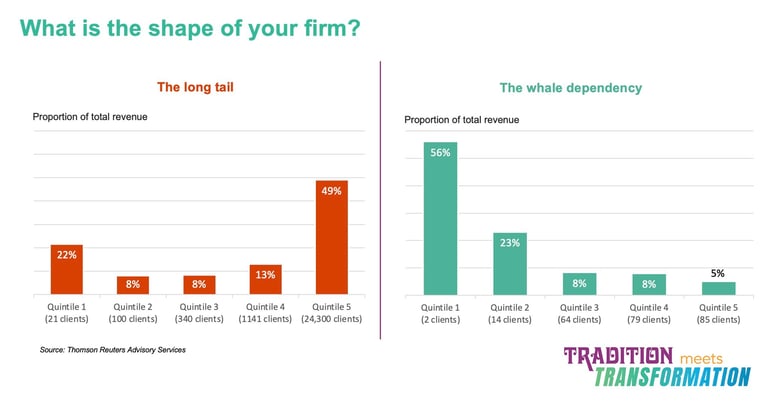

She introduced two analytical frameworks that any BI or CI team can apply to client financial data. The first is tail velocity. Most firms have a long tail of low-value, episodic client relationships that add activity but not momentum. The data consistently shows that most tail clients never graduate upward and many disappear entirely. Chasing growth in the tail is expensive and, more often than not, wishful thinking.

The second is share of wallet. Not all clients have equal growth potential. Firms often build client teams around relationships where they're already capturing 30-40% of outside counsel spend, or they chase prestige logos that spent a small amount once. The realistic sweet spot is with clients where the firm handles 10-24% of their legal spend. There's significant headroom, the client is financially engaged, and you don't have to displace deeply entrenched competitors to grow.

Jen closed by connecting this to AI. Once you know which clients to pursue, your AI strategy becomes critical to how they experience your firm. AI is becoming the lens through which clients evaluate efficiency, responsiveness, and commercial awareness. And the data shows that clients are rating firms poorly in exactly those areas. The role of marketing, BD, and intelligence teams is not just to respond faster to requests. It's to help leadership see where growth is real, where effort is wasted, and where discipline and differentiation create a genuine strategic advantage.

Quynh Skiven: The Data Foundation That Makes Everything Else Possible

Quynh Skiven is a data strategy consultant at Epiq and a former attorney. Her perspective is blunt: most firms' data infrastructure is not ready for the AI-driven future that everyone is excited about, and the cost of ignoring that is compounding.

She framed the problem through what she called the "dirty data drain," the largely invisible cost that accumulates when systems don't work together, records are duplicated or inconsistent, and data quality is treated as someone else's problem. The losses show up in time, money, and missed opportunities, but they're hard to quantify, which is part of why they get ignored.

Quynh put numbers to it. She cited research showing that 95% of AI pilots fail to deliver on their expected outcomes, and the root cause is almost always the data underneath, not the AI itself. Firms buy technology and layer it on top of messy foundations, then wonder why the results are disappointing. She also highlighted the growing penalties for AI-assisted citations in legal filings. The early stories about lawyers citing nonexistent case law were treated as embarrassing anomalies. Now, courts are imposing real consequences, and those penalties trace back to the same underlying problem: unreliable data feeding unreliable outputs.

She showed what the ideal state looks like: integrated systems, clean data flows, a shared understanding of what constitutes a "golden record," and a cultural commitment to maintaining data quality as an ongoing discipline rather than a one-time cleanup project. The gap between where most firms are and where they need to be is significant.

One of her most resonant points was about tech debt. She used an analogy that landed with the room: tech debt is like your phone's photo library. You ignore it until it becomes a crisis, and by then the cleanup is orders of magnitude harder than maintaining it would have been. In one client engagement, a firm spent six months on remediation work that could have taken one to two months if the right decisions had been made earlier. At another firm, the cleanup took more than three years.

Quynh also raised a stat that cut through the theoretical: 70% of new business goes to the firm that is first to reach out after a trigger event. If your systems can surface those triggers, whether it's a GC appointment, a regulatory change, or an executive move, faster than your competitors' systems can, you win the work. If your data is too fragmented to surface them at all, you don't even know you missed it.

Her Monday morning actions were deliberately small-scale. Identify your data silos. Define what a golden record looks like at your firm. Run an AI readiness audit, which she predicted would be an eye-opener for most firms. Automate one manual report, just one, to see how data flows through your systems and where it breaks. And start the internal marketing work: getting stakeholders across the firm on board with data strategy as a shared priority, not one department's project.

The cultural challenge was a thread she returned to repeatedly. She described working with clients where one department makes real progress on data quality, then hits a wall trying to expand the work across the firm. The barrier is rarely technical. It's organizational. Getting buy-in requires marketing the initiative internally with the same discipline you'd apply to an external campaign.

Robert Ambrogi: The Competitive Landscape Is Already Different

Robert Ambrogi is a legal technology journalist and the host of the LawNext Podcast. He has covered legal tech and innovation for decades, and his assessment was direct: the legal profession is at one of the most unprecedented points of change in its history, and most law firms are not adapting to it. Many haven't even recognized it.

To paraphrase Richard Susskind:

"Part of the problem with trying to tell lawyers that their business model is broken is that they are all millionaires."

For as long as law firms have existed, he argued, their only competitors were other law firms. That has changed fundamentally in the last few years, and AI is accelerating the shift. He outlined four categories of new competition.

AI-native law firms. These are not firms that have adopted AI as an add-on to their existing operations. They are being built from scratch with AI as the operating system. The most striking example: Blackstone, one of the world's largest asset managers and historically one of the biggest clients of elite law firms, spent more than $100 million in fees to Kirkland & Ellis alone in 2024. Blackstone has now invested $50 million in NormAI, an AI-native law firm, and is working directly with NormAI to train it on the kind of work Blackstone needs done. The former chair of Sidley Austin, Mike Schmidtberger, left to become NormAI's chairman in January 2026. Other signals: Garfield AI became the first AI firm approved by the UK Solicitors Regulation Authority to deliver legal services. Lawline, a Google-backed AI startup, acquired UK firm Woodstock Legal Services in what is believed to be the first known acquisition of a law firm by an AI company. And Y Combinator, the leading Silicon Valley startup accelerator, has been actively encouraging founders to start alternative law firms.

Management service organizations (MSOs). These structures separate the business of law from the practice of law. An investor-owned MSO handles marketing, technology, billing, data analysis, and all back-office operations. A separate, lawyer-owned firm handles the legal work. The model allows private capital to invest in law firm operations in a way that traditional ethics rules around non-lawyer ownership would otherwise prevent. McDermott Will & Emery has been publicly exploring this model. Burford Capital, a major litigation funder, has been as well. A new entity called Legensity recently launched as a consortium of large service providers forming an MSO to serve multiple firms. The implications for marketing, BD, and client relationships are significant, as these functions move into a different entity with different incentives and governance.

Alternative legal service providers (ALSPs). ALSPs emerged after the 2008 financial crisis, combining legal skills with technology to deliver commoditized services like discovery review and contract review more efficiently and at lower cost. The "alternative" label barely applies anymore; they have become mainstream. Thomson Reuters and others project continued significant growth in this market, accelerated by AI capabilities.

In-house legal departments. Corporate legal teams have been growing in sophistication and size for years, steadily bringing more work in-house. AI is accelerating this trend. Ambrogi noted that vibe-coding, using AI to build simple applications without deep technical expertise, is enabling legal departments to create their own workflow tools and reduce dependence on outside counsel for routine work.

After laying out the competitive landscape, Ambrogi turned to the financial picture. On the surface, the numbers look healthy: 7.4% work rate increase, 6.6% revenue-per-lawyer growth, 13% profit growth. But beneath those headlines, the story is different. 64% of firms are reporting declining billable hours. Write-offs are up sharply. Aged work-in-progress is now the number one cash flow pressure at half of all firms. Clients are shifting work downstream. Mid-sized firms are growing faster than the Am Law leaders.

He called this the "boiling frog" scenario. If you drop a frog in boiling water, it jumps out. If you put it in water that's slowly heating, it sits there. Firms are sitting in water that's getting warmer. Hours are declining, but targets keep rising. Write-offs are surging, but rates keep climbing. Clients are migrating, but revenue still looks fine. Partnership meetings are focused on last year's performance when they should be focused on next year's reality.

The fundamental tension, Ambrogi argued, is that firms are adopting AI to do work faster while still building their entire business model around billing by the hour. That is unsustainable. Something has to break.

His priorities for firm leadership: audit which practice areas are most vulnerable to the changing competitive environment, particularly commoditizable, repeatable services that AI-native firms and ALSPs can deliver at far lower cost. Overhaul pricing strategy and stop relying exclusively on the billable hour. Think about whether your firm is a platform or a practice. Formalize AI governance before clients force you to. Invest in data as a strategic asset. Break down internal silos. And watch the client, not just the competition, because what your clients expect from you is changing faster than what your competitors are doing.

Where This Leaves Things

The session closed with a prediction round and audience discussion. A question from the audience about Harvey, the AI legal technology company whose valuation now outstrips what law firms spend on their total technology budgets, prompted Ambrogi to note that Harvey has embedded itself carefully into firm workflows over three years, positioning as a partner rather than a competitor. But he observed that AI-native law firms are essentially building Harvey-like capabilities natively around specific practices. The platformization of law, whether through companies like Harvey or through AI-native firms themselves, is already underway.

The through-line across all three speakers was consistent. Jen showed that the growth story firms tell themselves is more fragile than the headline numbers suggest, and that disciplined client analytics, not lateral hiring, is where sustainable growth lives. Quynh showed that none of the AI-driven future works without clean data, integrated systems, and organizational buy-in. Bob showed that the competitive landscape has shifted in ways most firms haven't internalized, and that the window to adapt is shorter than it feels.

The session was designed to be provocative, and it delivered. As one attendee put it during the closing discussion: the challenge isn't convincing a room of data and intelligence professionals that this matters. The challenge is that the people who most need to hear this are in partnership meetings focused on last year's numbers.

This post is part of a series from the LMA 2026 Annual Conference Pre-Conference Program, "AI, BI, CI: The ABCs of Data and Law Firm Intelligence," co-chaired by Michelle Woodyear (Mount Insights), Ashley Elliott (FBT Gibbons), and Rafeedah Keys (Perkins Coie). The e-book "The AI-Enabled Legal Marketer" and the guide "Free CI Research Tools" were shared with attendees of the pre-con session.